Retail investors in India look for alternatives to traditional bank deposits for a fixed income investment. NCD IPO enables people to lend money to large corporations at a certain interest rate. This process makes the corporate debt market accessible to all. Investors usually favour them since they provide definite returns and less risk compared to the stock market.

What is NCD IPO?

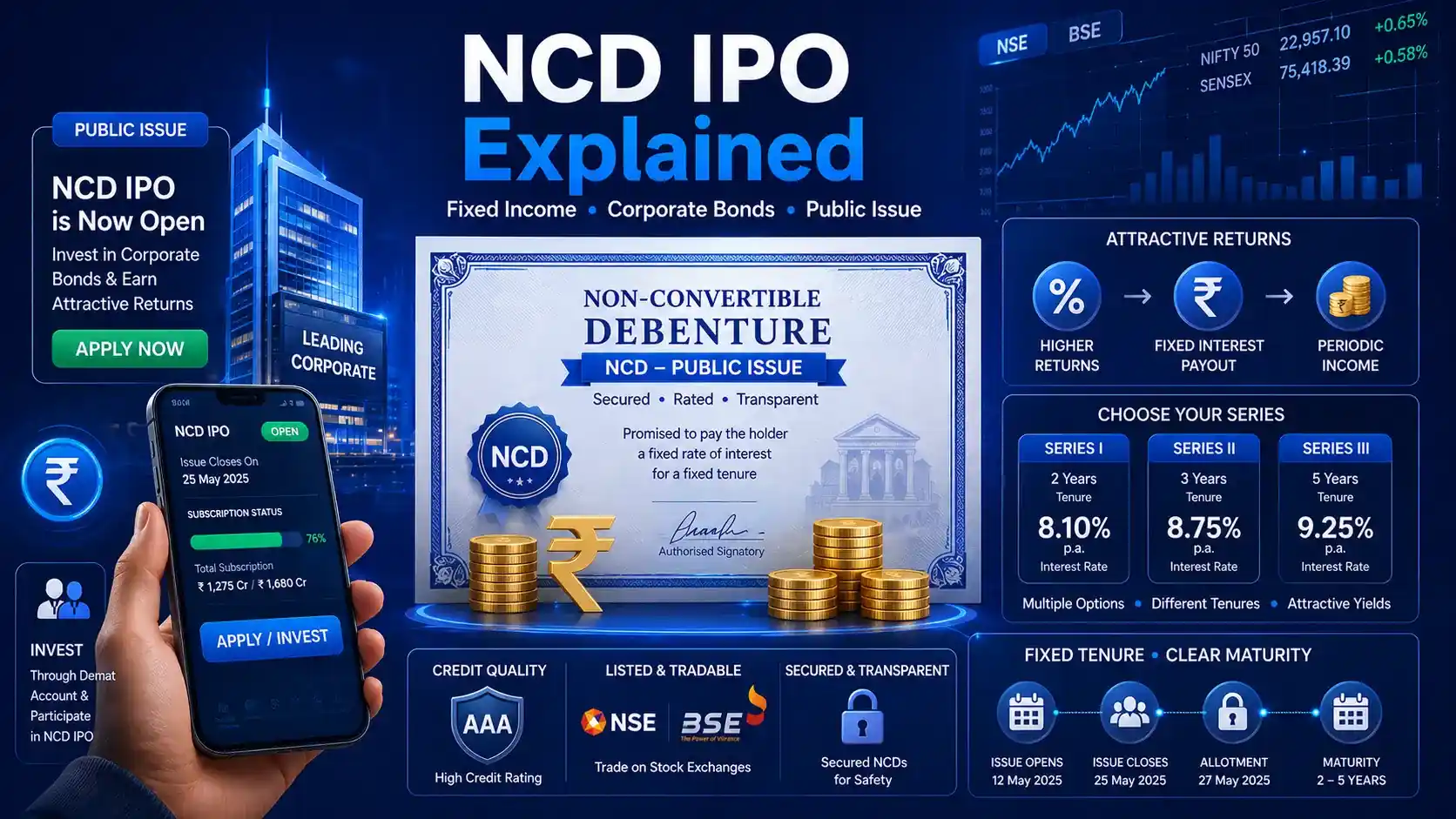

Non-Convertible Debentures (NCDs) IPO issues are the methods used by companies to raise capital to fund their business needs. A company is able to issue an NCD IPO more than once in a year, unlike a regular stock IPO, in order to raise more money.

Features of Non-Convertible Debentures NCD IPO

- Fixed Returns: The companies will offer to pay a specific interest rate to the investors. This rate does not change during the investment tenure.

- Multiple Series: Investors can have various options in one NCD IPO. Every alternative comes with its own time frame and interest rates.

- Debt Nature: The investor is turned into a lender to the company. At the expiry of the term, the company will need to pay the principal amount.

- Public Access: The general public can apply for these bonds using their demat accounts. Retail participants find it a very easy process.

- Capital Raising: Businesses use this mpney to grow their business or settle old debts. The NBFCs normally manage their cash in this manner.

Major Smart Investor Terms

The debt market has a set of words that are used to describe the type of investment made by investors. These words define your rights and the worth of your investment.

- Face Value – This is the original price of one single NCD. The majority of companies set this at 1,000 rupees per unit.

- NCD Holder – You become a holder when the company assigns you the bonds. You are not an owner, but a creditor of the company.

- Debenture Redemption Reserve – Companies used to keep a separate cash reserve to ensure repayment. Modern rules now exempt many large companies from this strict requirement.

- Overall Issue Size – The term is used when a company is not using a shelf prospectus. It is the total value of the particular bond offer.

- Redemption Date – This is the maturity day on which the company pays back your initial investment. You stop earning interest after this specific date.

NCD IPO Official Paperwork

Each NCD issue needs specific legal documents that detail the rules of the investment. These documents inform you about the precise amount of money that the company wants and how they will pay you back.

- Shelf Prospectus: This is a master file of all issues to be planned in a year. It includes all the historical background: information of the company and its finances.

- Tranche Prospectus: This particular document is issued by the company whenever a particular round of funding is undertaken. It includes the specific interest rates and dates for that particular issue.

- Shelf Limit: This is the maximum total money a company can raise under one master document. The company will not be able to cross this limit without filing new papers.

- Base Issue Size: This number shows the minimum amount of money the company aims to collect. It is the starting target of the public issue.

- Green Shoe Option: When there are more applicants than the target size, companies can keep additional money. When the demand is high, they usually retain up to double the base amount.

- Tranche Issue Limit: This is the final size of an individual issue after adding the extra demand. It should not exceed the total shelf limit of the company.

NCD IPO Interest Rates and Payout Methods

Interest income is the primary reason why people purchase NCDs. You have the option of deciding on the frequency at which you wish to receive your money based on your own needs.

- Coupon Rate: It is the interest rate that the company pays you annually. Until your bond matures, it is the same.

- Monthly Payout: The company send interest to your bank account on a monthly basis. This is helpful for people who need a regular monthly income.

- Annual Payout: Investors are paid their overall annual interest after every 12 months. This helps in planning big annual expenses or taxes.

- Cumulative Option: The interest is re-added to the principal amount. You get a large lump sum only at the very end.

- Effective Yield: This indicates the true profit percentage after taking into account the effect of compounding. Cumulative plans usually show a greater effective yield to investors.

Special Features and Exit Options of NCDs

Some NCDs come with extra benefits or special conditions for early exit.

- Incentive Rates – Companies often give extra interest to their existing shareholders. This reward encourages loyalty among the current investors of the company.

- Call Option – The company has the option of repaying the money prior to the final date. They tend to do so if market interest rates fall significantly.

- Put Option – The investor can request the refund of his/her money prior to the maturity. This is not a common aspect and often comes with a lower interest rate.

- Day Count Convention – This is the mathematical equation to calculate interest for broken periods. It makes sure that you earn interest every day that you own the bond.

- Holiday Adjustments – When a due date falls on a bank holiday, payments may be made a day later. The company has stringent regulations to make sure that investors do not incur losses.

Conclusion

NCD IPOs are a good option for individuals looking for better returns as compared to traditional savings. You earn more interest and have a clear repayment schedule. You should never invest your hard-earned money without first checking the credit rating and the prospectus. Such investments are useful in the building of a diversified portfolio with a stable flow of income.

No comments yet. Be the first to share your thoughts!